"provides exploration and production services to the offshore oil and gas industry building on 150 years experience in shipping and more than 35 years in offshore drilling."

Byford Dolphin oil exploration rig in dry dock at Invergordon (Scotland) on 2008 (source: User Jetset / Wikipedia)

{kind=link}

We have had that stock now over 2 years in the portfolio. At the time of writing it had closed at 255 NOK about +44% above our purchase price of 176,50 NOK in Oslo Børs (stock exchange of Oslo, Norway). The yield has been good. They have paid 20 NOK dividend per share this year and last year making the yield 11,3% p.a. for the original investment. However, the company has stated to pursue strategy to pay a dividend of NOK 10 per share. In the last two years the company has paid extraordinary dividend of NOK 10 per share. A concervative future yield estimate is thus to be calculated with NOK 10 per share meaning 3,9% yield at NOK 255 stock price level.

Market cap of the company is NOK 17 billion (about USD 3 billion). P/E (2011) is 8,2. This assumes net result after tax to be NOK 2083 million (result for 2011). The company has been making about NOK 2 billion net result for last 5 years except for 2009 (2,7 billion) and for 2007 (1,4 billion). Nordnet gives the following financial figures for current share price of NOK 255:

- ROE 28%

- P/E 8,7

- P/B 2,4

- P/S 2,8

Net cash flow from operating activities look good. However, the company has been making sizable investments in 2Q 2012 and therefore net change of cash has been negative. Dividend of 1325 million NOK paid in Q2 2012 is less than net cash flow from operating activities from 1H 2012 alone (1606 million NOK) so even the elevated dividend level of NOK 20 does not look high compared to cash flow.

The Company, subsidiaries and major owners

Fred. Olsen Energy ASA, headquartered in Oslo, Norway, is a holding company and provides management services to the subsidiaries within the Group:

Fred. Olsen Energy ASA, headquartered in Oslo, Norway, is a holding company and provides management services to the subsidiaries within the Group:

- Dolphin Drilling AS (HQ Stavanger, Norway, 100% owned)

- Dolphin Drilling Ltd. (HQ Aberdeen, Scotland/UK, 100% owned)

- Harland and Wolff Group Plc. (HQ Belfast, Northern Ireland/UK, 92.2% owned)

The drilling segment delivers practically all of the net result. The Engineering & fabrication segment (Harland and Wolff) is small in comparison.

The Dolphin Drilling companies form the drilling contracting business activities of Fred. Olsen Energy ASA.

"Dolphin Drilling is one of the longest established independent drilling contracting companies in the offshore arena tracing its roots back to the earliest offshore exploration activity in the North Sea in the mid nineteen sixties. The Fred Olsen family’s interest pre-dates this with a history in shipping activity stretching over 150 years."

The Olsen family is a major shareholder (53.4%) via their holding companies:

The Fleet

{kind=link}

{kind=link}

{kind=link}

Fleet summary. Information from company web site and annual report 2011.

The offshore fleet of Fred. Olsen Energy ASA with subsidiaries consists of two deepwater units and six mid-water semi-submersible drilling rigs in addition to one accommodation unit. The Group has two newbuilds under construction, an ultra deepwater drillship scheduled to be delivered in 3Q 2013 and an ultra deepwater semi submersible for harsh environment scheduled to be delivered in 1Q 2015.

Contractual situation looks pretty good. There are long contracts for both drill ships with Anadarko Petroleum Co. There is also long contracts for Byford Dolphin and Borgsten Dolphin. Rest are ending between Q4 2012 and Q1 2014 according to company web site.

{kind=link}

It's worth to note that Blackford Dolphin, the deep water semi-submersible drilling rig, was estimated to be worth 3459 million NOK at end of 2011 according to annual report. Alone that's about third of net book value of all their rigs and drillships. Basically over half of assets were tied to two deep water units and the ultra-deep water Bolette Dolphin drill ship under construction at end of 2011. With the ultra-deep water semi-submersible drilling rig targeted to be finished 2015 the company will have significant portion of company net assets in the deep water and ultra-deep water segments.

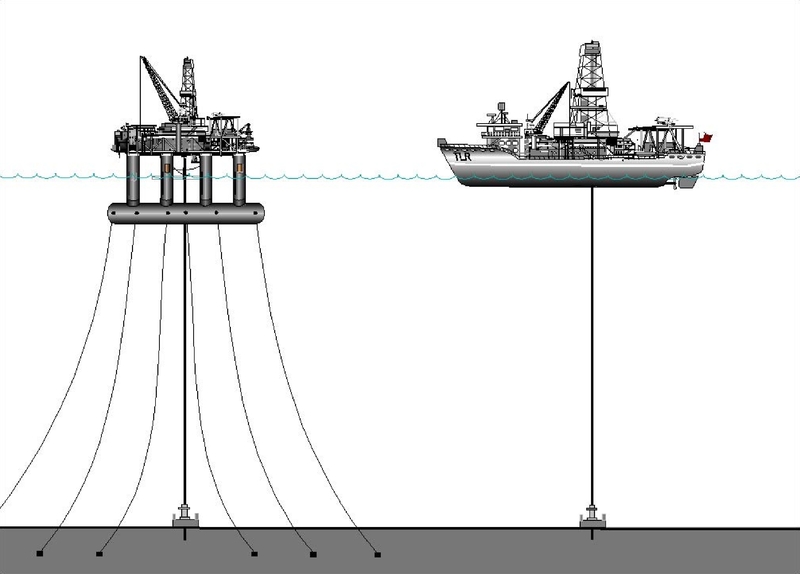

The definition of "deep water" seems to vary in the industry and has shifted over the years with technical advances. This company considers 1000-1750 feet mid-water, while U.S. government definition of deep water shifted from 1000 feet to 500 feet after Deepwater Horizon -accident in Gulf of Mexico. The 500 feet limit seems to come from the fact that the intervention in the well at the seafloor switches from divers to Remotely Operated Vehicles (ROVs) at about 500 feet. A government report from UK concluded this also to be an obvious threshold for deep water operations. According to this definition all the the assets of Fred Olsen Energy are "deep water" or "ultra deep".

Regardless of the definitions, it seems that the offshore oil exploration and production is moving to ever deeper depths. An interesting perspective is that 162 year old oil industry started deep water exploration in 1975 and production 20 years later in 1995. Anyway, deep waters is where the day rates are today the highest and that's also where the demand increasingly is likely to be for drill ships and rigs.